Electronic payment systems as a field of study have become important with the recent rise in e-commerce activities taking place on the internet to help conduct faster, secure, and large-scale payments successfully. An electronic payment system, by definition, is a mode of payment that facilitates acceptance of electronic payment primarily for commercial transactions over the internet. Any electronic payment system must involve three key types of stakeholders—the payer (consumer), the payee (business or merchant), a financial network (with which both payer and payee have accounts).

Traditionally, payments used to be made through cash, cheques (using ‘clearinghouse’ between banks), and Giro (direct credit and debit transfers). But with the advent of internet and electronic transactions, multiple types of new payment models have emerged, the most prominent among them being credit card payments, electronic cash (also known as e-cash), electronic checks, and smart cards. Let us understand all of these four in more details.

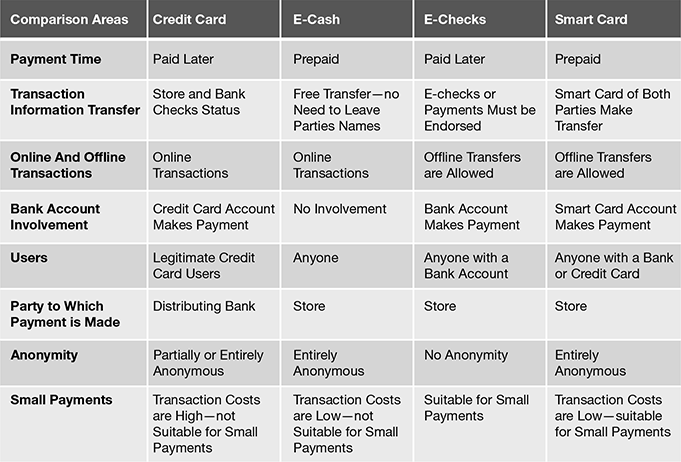

- Credit card payment: Credit card transactions take place over large electronic networks, typically linking cardholders, merchants, card-issuing banks, merchant banks, and credit card companies.

- E-cash: Credit card transaction fees, typically, make small purchases unprofitable. Electronic cash, which is cash converted into electronic form, improves upon paper cash since the security and privacy features offer more efficient means of cash payments. E-cash, typically, have not been that popular for reasons of lack of standards and interoperable software.

- E-checks: An e-check is an electronic version of the paper check and is a payment instrument which was developed by a collaboration of several banks, government entities, technology companies, and e-commerce organizations to provide highly secure, speedy, and convenient online transactions.

- Smart cards: These are plastic cards containing an embedded microchip that contain important financial and personal information which can be periodically recharged and helped with very small transactions.

In their article ‘An Analysis and Comparison of Different Types of Electronic Payment Systems,’ authors Zon-Yau Lee, Hsiao-Cheng Yu, and Pei-Jen Kuo shared an elaborate comparison of these four electronic payment system types (see Fig. 9.3).

Figure 9.3 Comparison of Electronic Payment Systems

With an understanding of the four global electronic payment system types, we would now look at the key electronic payment and settlement systems in India. The RBI (Reserve Bank of India) has played a key role in making it compulsory for banks to route high value transactions through Real Time Gross Settlement (RTGS) and has also introduced NEFT (National Electronic Funds Transfer) and NECS (National Electronic Clearing Services) which has encouraged individuals and businesses to utilize electronic methods of payment. Let us understand some of these payment methods:

- ECS (Electronic Clearing Service) Credit: Known as ‘Credit-push’ facility or one-to-many facility, this method is used for large-value payments where the receiver’s account is credited with payment from the institution making the payment.

- ECS (Electronic Clearing Service) Debit: Known as many-to-one or ‘debit-pull’ facility, this method is used mainly for small value payments from consumers/individuals to big organizations or companies.

- RTGS (Real Time Gross Settlement): It is a funds transfer mechanism where transfer of money takes place from one bank to another on a ‘real time’ and on ‘gross’ basis.

- NEFT (National Electronic Fund Transfer): A nation-wide system that facilitates individuals and firms to electronically transfer funds from a bank branch to any individual or corporate having an account with any other bank branch in the country.

- IMPS (Immediate Payment System): It is a service through which money can be transferred immediately from one account to another, within the same bank or accounts across other banks.

Leave a Reply